Skip to content

Skip to content Earlier this year I shared my superannuation balance online and to my surprise more than 20,000 people viewed it on red note. Many readers said they picked up something new or felt inspired to think about their own super performance, which is extremely and impactful as it is going to be a foundation for one’s retirement.

This is my journey as a peasant working an average 9-5 trying to grow wealth through superannuation, ETFs and property. I hope that if you stumble on this article, you can find something useful along the way.

Taking Super Seriously

I only started taking my super account seriously three years ago. By planning my daily expenses better and making extra contributions, I managed to put more into super plus get a juicy tax return along the way. The two key benefits of this extra contributions are:

Tax savings – super contributions are taxed at a lower rate (15% vs marginal tax rate), money within super churning out investment returns are also taxed favourably

Long-term returns – super allows my money to compound in a tax effective environment, it reduces behaviour risk to an extent as well compared to a normal brokerage account where I can YOLO into some meme stock

Working in wealth management, I’ve seen many clients accumulate significant wealth through their super. That gave me a first hand appreciation for the power of the system.

My 10-Year Super Performance

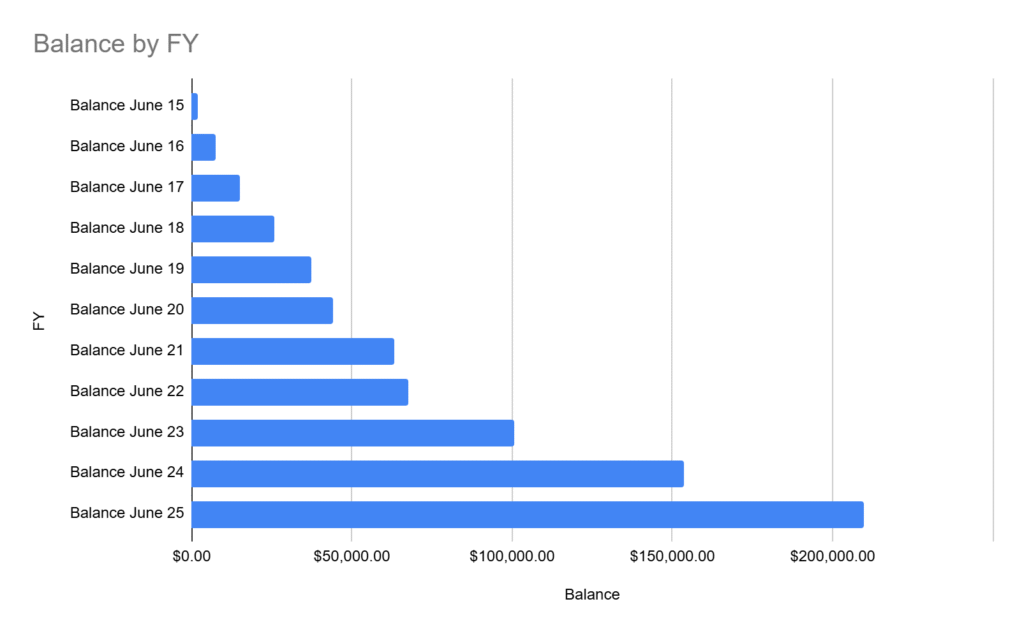

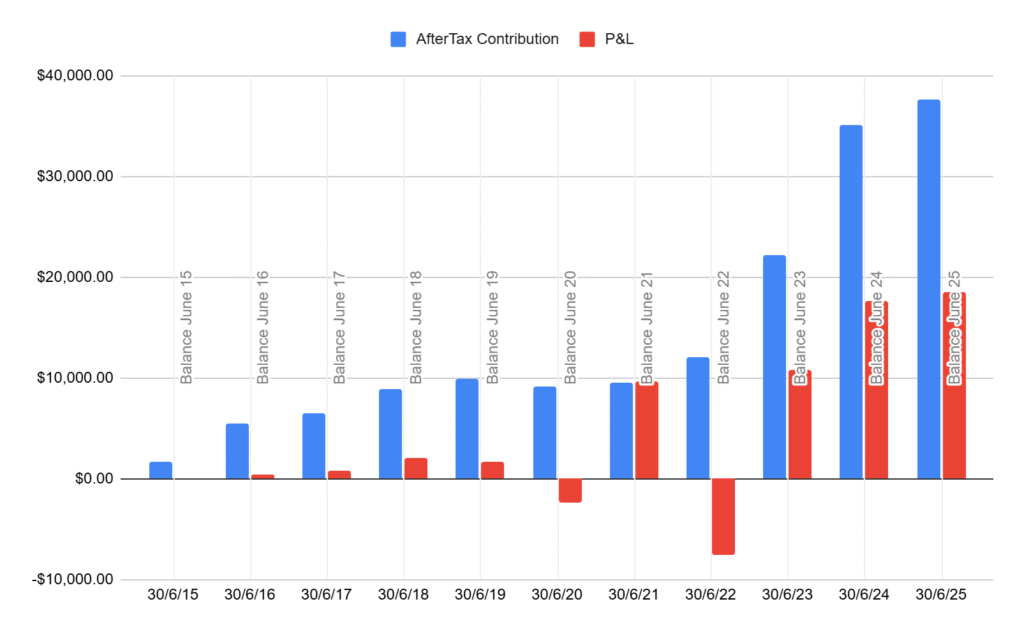

Here’s the data as of FY25 (30th June):

Total after-tax contributions: ~$158,000

Current balance: $209,655

Earnings from super: $51,500

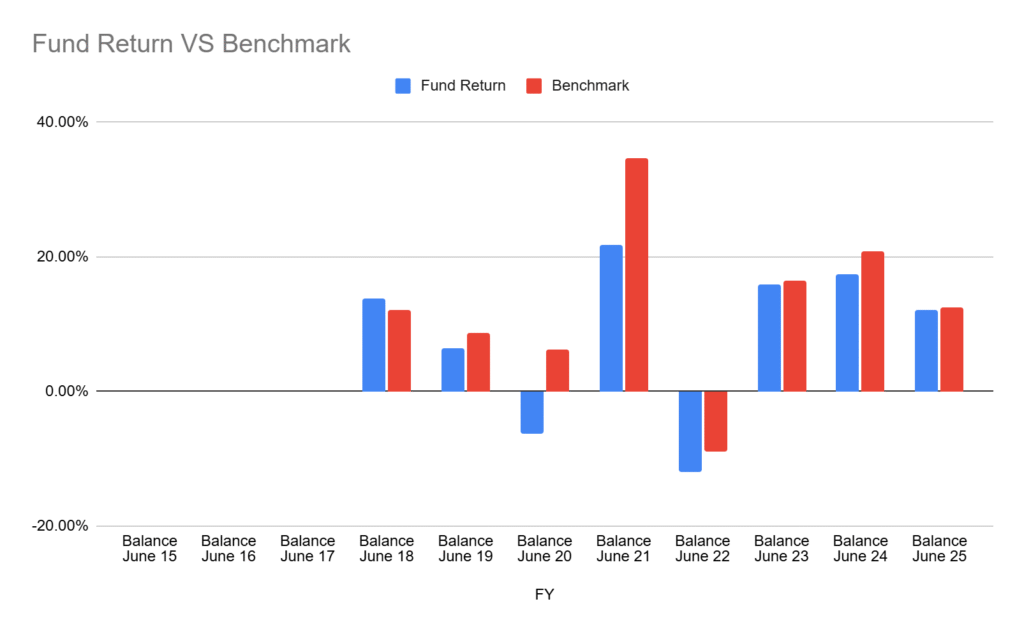

MWRR (market weighted return): 9.17%

Total return: 32.6%

FY25 performance: 12.08% / +$18,500

Seeing these numbers makes me genuinely happy, I can feel the power of compounding returns over time. Without any additional effort, my money has been generating more year on year! (see chart below)

My Current Super Investment Approach

As of June 2025, around 85% of my super is invested in international equities with roughly 40% in currency hedged options. However as of writing this article, Hostplus decided to shutdown the “international hedged index” option which is a real shame…

For those wondering what “hedged” means, it simply removes the impact of currency fluctuations on returns. For example, for the last few years investing in unhedged international ETFs would have generated more return compared to the hedged counterpart due to AUD falling in value. On the other hand, if the Australian dollar rises or the foreign currency drops, the hedged option would outperform.

That said, I think I may have over-allocated to hedged options. In FY25 it didn’t add much extra benefit till the latter few months in the financial year. I will likely reduce currency hedged allocation to around 20-30% going forward.

Lessons from Watching Others (and Myself)

Something I’ve noticed while talking with friends is that many people pick too many super options, making it hard to know what they’re actually invested in. Or the polar opposite, they don’t even know what they are invested in.

Here’s a quick tip: just log in to your fund’s website and check whether you’re in High Growth, Growth, Balanced or Conservative. These preset mixes are mainly just different allocations between equities and bonds. Pick one that suits your risk profile and life stage, then stick with it. Noting these pre-mix options are typically actively managed meaning higher management fee. I prefer the passive/indexed options but that may take some further due diligence.

The truth is, investing has no absolute right or wrong. What matters is consistency and alignment with your personal risk tolerance. I reckon that I tinkered a bit too much this year and honestly, it didn’t outperform the market. Super is not a get-rich-quick scheme. It’s a long-term wealth-building tool and if you keep contributing, stay disciplined and let compounding do its work, time will take care of the rest!