Skip to content

Skip to content “What was your superfund’s return over the years?”

I asked myself this question two years ago. The answer surprised me and changed the way I think about my retirement savings forever.

The Early Years: High Fees, Low Awareness

When I started working a decade ago, superannuation was just a line on my payslip that I never paid attention to. I was setup with AMP and like many people, I just went along with it. At the time, I had zero investment knowledge and funny enough what I did was jump from one “top performing” fund to another every couple of months. I thought I was being proactive but in reality, I was just performance chasing—without understanding the fees, tax implications or what the funds were actually investng into.

Looking back, those early years taught me a few painful lessons:

Active funds often look good during short bursts of outperformance, but very few deliver consistently.

Higher fees, switching and platform costs eat into your returns quietly but significantly.

Switching funds frequently can trigger unwanted CGT, especially on wrap platforms.

The Wake-Up Call: FY2020 – FY2021

The market bounced back aggressively after COVID and FY21 turned out to be one of the strongest years in recent memory. The S&P500 was up more than 30% and even Australian equities performed well. BUT! My superfund returned a lot less than that.

I didn’t even notice at the time. There were no bells or alarms going off as I looked into the numbers and was busy grinding the full time job. But when I later compared the data and tracked it side by side with the market, I realised how much I had left on the table. That year alone, the performance gap between my active fund and a plain index option was nearly 12%. That was my turning point.

Mindset Shift: Indexing, Simplicity and Tax Planning

I eventually switched my super over to Hostplus with a mix of indexed options, with total admin fees of around $78/year and investment MERs that are very low. In FY23, I also started contributing more deliberately into super, taking advantage of concessional contributions to reduce my taxable income.

Check out this illustration. Let’s say your marginal tax rate is 30%:

Every $1 you contribute to super only gets taxed at 15%

That’s an instant 15% “return” on your money, just for using the system right

Sure, that money is locked until retirement age but it is your money afterall and if you’re thinking long term, it’s one of the best risk-free “returns” available.

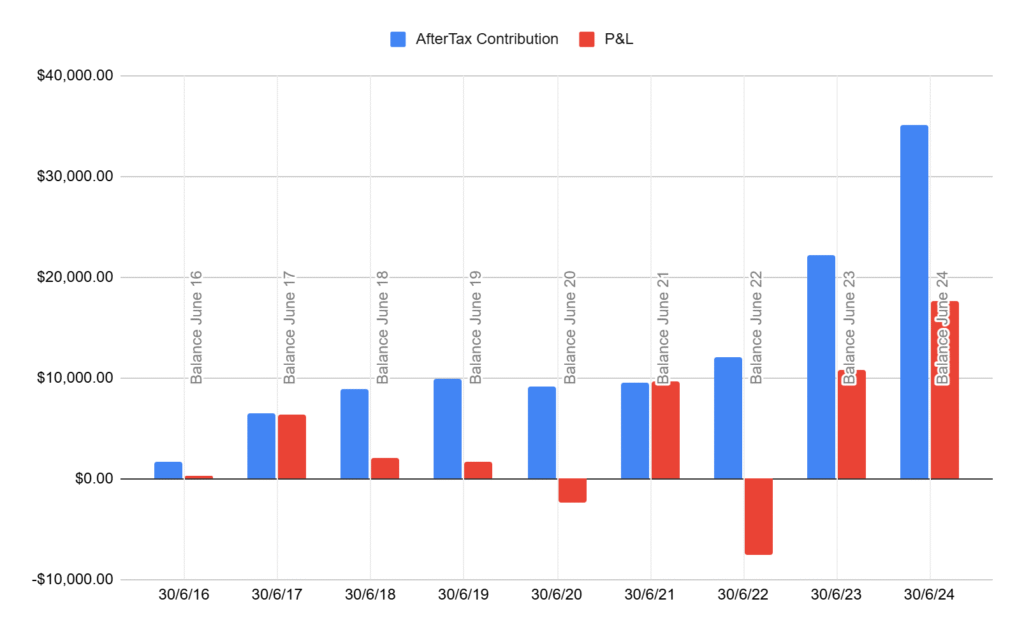

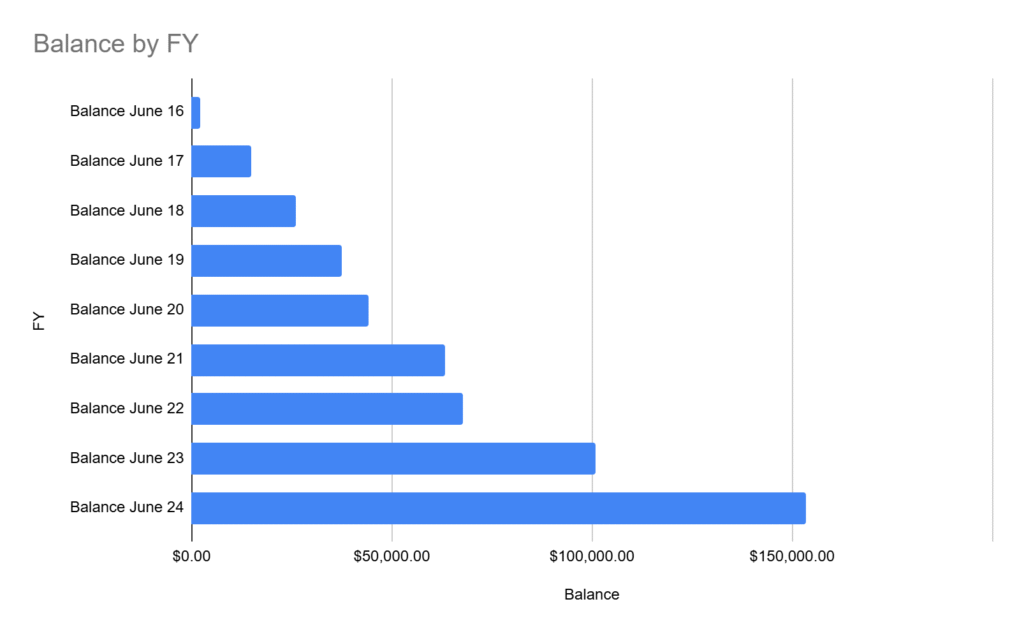

9 Years of Super Performance

Here’s the summary of my personal journey:

Total post-tax contributions: ~$115,000 (87k from employer and 28k of my own contribution)

Super balance (end FY24): ~$153,500

Investment gains over time: ~$38,500

Market weighted return (annualised): 9.63%

Not terrible, but not exceptional either—especially when you factor in the lost opportunities during my active fund chasing phase.

The Takeaway

You don’t need a super high salary to grow your super. You just need to:

Understand your fund options (active vs index, fees)

Avoid unnecessary switching and performance chasing

Use concessional contributions strategically for tax savings

I’ve had chats recently with friends and colleagues who earn far more than I do. Some have never even checked their super performance. That’s wild, considering it’ll likely be one of the biggest assets they retire with.

So if you’re reading this and haven’t looked at your super in a while, maybe it’s time to start. Track it. Compare it. And ask yourself: is your money working as hard as you are?

Coming Soon: FY25 Performance Update

I’ll be updating my super numbers again in July once the annual report drops. If you’re interested in comparing notes or starting to track your own journey, stay tuned!

Note: Benchmark data used is the price return of S&P500 during this time as I do not have the data for the total return.